D-Fend: Before the Category Existed. Our Investment & Journey with D-Fend

Yoram Oron07 Jul 2026/f/233941/1918x1080/ca39eef39f/dfend-hero-image.png)

Introduction

Forty years ago I started a defence company. This was the late 1980s, and the idea was almost absurd at the time. You could raise money then for the early promise of computing and, a little later, for the internet. You could not raise money for defence.

The category did not interest people, and what little interest existed came wrapped in suspicion. I raised it anyway, sold the business to a public company, and ended up running that public company as its chief executive.

I tell you this not to recite a resume, but because it explains why, some thirty years later, I was able to sit across a table from three engineers describing a problem most investors did not yet believe was a problem — and recognise immediately what I was looking at.

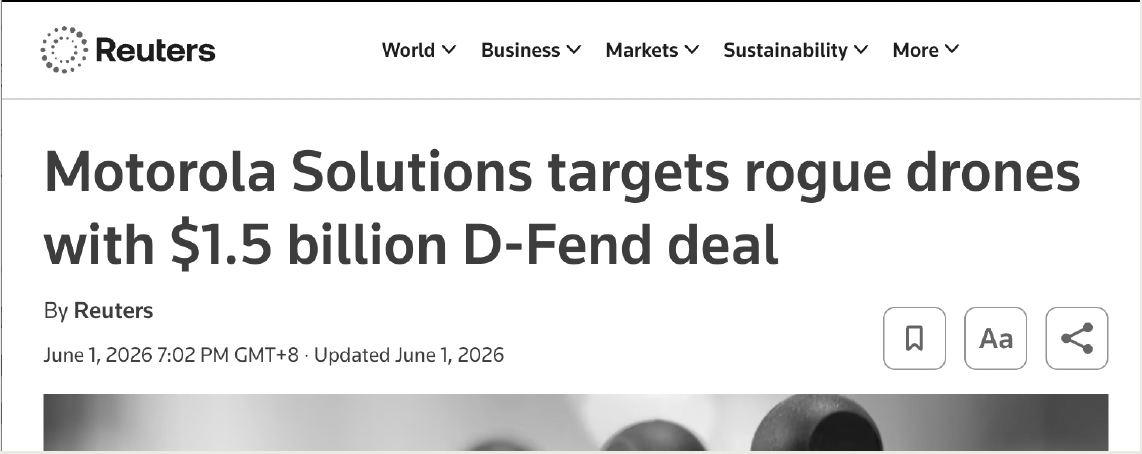

The company was D-Fend Solutions. The problem was drones. In June of this year, Motorola Solutions agreed to acquire it for 1.5 billion dollars.

“It was not obvious. For most of the journey it was the opposite of obvious.”

D-Fend founders — Zohar Halachmi · Assaf Monsa · Yaniv Benbenisti

D-Fend founders — Zohar Halachmi · Assaf Monsa · Yaniv Benbenisti

01 — The Need and Its Alternatives

The First Meeting

I am an electronic engineer by training. I graduated from the Technion many years ago, and before I was ever an investor I built things and sold them and lived with the regulators who govern this world. So when the founders walked me through what they intended to build, I was not learning the field from scratch.

I could follow the need — always the first thing I try to understand — and I could follow the alternatives to that need. Those two questions are where most investments are won or lost long before the spreadsheet is opened.

The need was clear once you let yourself see it. Drones were becoming cheaper, more capable, and far harder to manage in places that cannot tolerate disruption. An airport. A stadium. A city centre. A power station. You cannot shoot a drone out of the sky above a crowd, and you cannot jam every signal in a busy airport without grounding everything else.

The founders’ answer was not destruction but control: detect the drone, identify it, take it over, and land it safely — without broad jamming and without collateral damage.

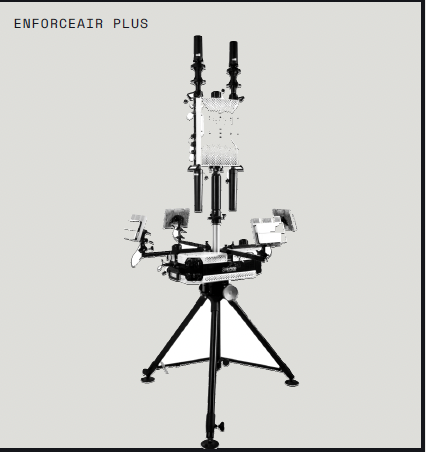

EnforceAir Plus — cheaper, more capable, everywhere. Detect → Identify → Take Over → Land.

EnforceAir Plus — cheaper, more capable, everywhere. Detect → Identify → Take Over → Land.

“When the customer tells you the problem is real even as they doubt the solution, you are in a very interesting place.”

02 — The Lazy Arithmetic

What the market got wrong

Eight years ago, and for some time after, investors looked at a company like D-Fend and reached for the wrong comparison. They compared it to cybersecurity, to communications, to enterprise software — all serving commercial markets with clean economics.

Eight years ago, and for some time after, investors looked at a company like D-Fend and reached for the wrong comparison. They compared it to cybersecurity, to communications, to enterprise software — all serving commercial markets with clean economics.

On paper those businesses carried multiples of twenty or thirty times. Defence companies traded at three to five. The arithmetic alone told investors to stay away.

The arithmetic was lazy. D-Fend was not enterprise software with a defence label. It was detection — hardware and software together — built to military specifications, in a sector heavily regulated even in the United States.

There was also the matter of time. The sales cycle for this kind of hardware can run two years; enterprise software can close in a month. Investors convinced themselves the wait was a flaw in the business. It was the market.

03 — The Cruelest Place a Startup Can Sit

The moments we nearly didn’t survive

People assume that a company which ends in a billion-dollar exit must have travelled there in a straight line. D-Fend did not. More than once we reached a junction where the board had to ask the hardest question a board can ask: do we keep going, do we sell the intellectual property, or do we wind it down.

We had product that worked and customers who valued it, and we still could not always raise the next round easily. That is the cruelest place a startup can sit.

What kept my conviction steady was a simple observation. Software and cyber companies routinely raise hundreds of millions before reaching cash-flow neutrality. D-Fend, through all of this, had raised on the order of 40 million dollars in total.

The amount at risk was modest relative to the opportunity, and that asymmetry let us keep going when the conventional doors were closed. The founders balanced R&D against the conservation of cash with a discipline that is rare — for years.

~$40M — Total raised across the entire journey, a fraction of a typical software burn. Evidence the problem was real, and a market not yet mature enough to underwrite it.

04 — Selling from Strength

Why we sold, and why now

About two years ago, when the company had finally moved past most of its risk, I went to my limited partners and invited them in at a valuation that ultimately delivered them roughly eight times their money — among them our sister fund, Vertex Growth.

About two years ago, when the company had finally moved past most of its risk, I went to my limited partners and invited them in at a valuation that ultimately delivered them roughly eight times their money — among them our sister fund, Vertex Growth.

I do not bring LPs into a deal to be polite. I bring them in when I believe the remaining risk is asymmetric in their favour, and only then.

When the time came, we had three bidders actively at the table. But the number is not what I optimised for — I was looking for a home: can the company keep growing under the new roof, keep its operation intact, keep most of its people.

Motorola Solutions is a 99-year-old public safety company. Under that brand and balance sheet, a customer will take a larger risk on the technology than they would on a startup — and the mission of protecting the skies will move faster and reach further.

05 — Inside the Revolution

What this exit says about the next decade

I have been saying for several years that the world has changed — that this sector has become not just acceptable but necessary. If you want to protect your country and your assets, you have to invest in this capability. That is no longer controversial, though it was when I wrote the first cheque.

Startups, when they are genuinely good, are faster than large companies at developing communications and inexpensive sensing. If you are two or three years ahead and able to execute, you hold real value for the incumbents who will eventually need it.

This was true of gaming, of the internet, of cloud, of artificial intelligence. It is now plainly true of public safety and defence — and it can be both very successful and quite profitable, which is, after all, what we as investors are after.

D-Fend was early to all of this: before the category was fashionable, before the multiples made sense to a spreadsheet, before the rest of the market caught up. That is the part outsiders miss when they read the headline.

The outcome was not the discovery of an obvious opportunity. It was the reward for conviction held through years when conviction was the only thing we had.

Yoram Oron

Founder & General Partner · Vertex Ventures Israel